Your Complete Guide to FICO Score

Mar 21, 2024 By Triston Martin

The Fair Isaac Corporation names a FICO score, which serves as a creditworthiness measurement tool based on an individual's credit history. Lenders extensively use this score to evaluate the risk of lending money to borrowers. Managing personal finances effectively and making informed decisions related to credit necessitate a crucial understanding of FICO scores.

The Components of a FICO Score

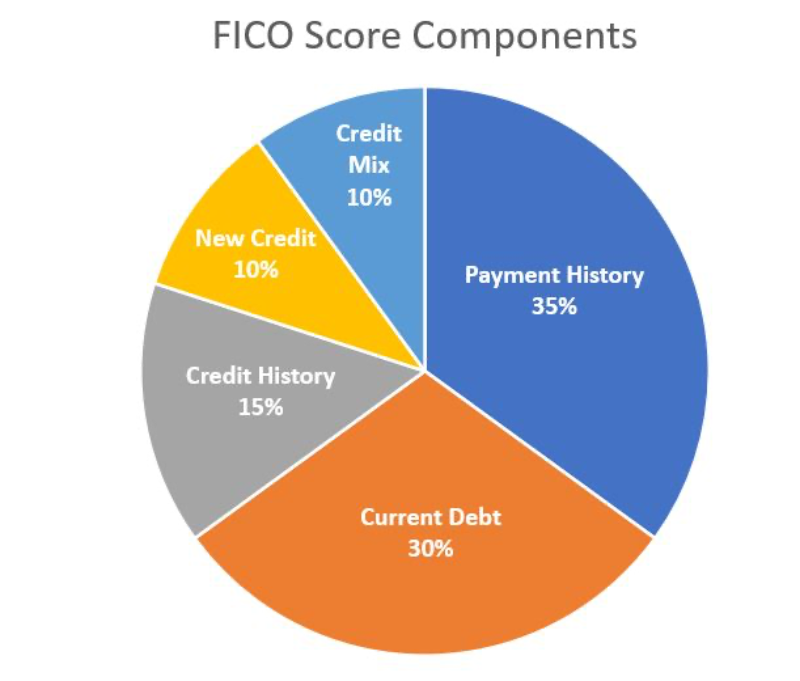

Various factors from a person's credit report calculate the FICO score such as payment history, amounts owed, length of credit history, new credit, and types of used credits. Determining the score is worth noting that payment history carries substantial weight followed by the amounts owed. Individuals can prioritize their financial habits and enhance their creditworthiness by understanding how these components influence their scores.

Considering the components of a FICO score necessitates an in-depth exploration of the significance of each factor. Notably, payment history not only mirrors your capacity to repay debts but also serves as evidence for your reliability as a borrower. Over time, consistently maintaining records of on-time payments can yield significant boosts to your overall score. Your credit history's length vividly illustrates your proficiency in managing credit accounts with responsibility. New credit and the types of credits used exert a lesser influence, yet they still shape your overall score. Hence, sustaining a portfolio that is both diverse and manageable can substantially enhance your FICO score.

- Credit Utilization: Keeping credit card balances low relative to your credit limit can improve your FICO score.

- Credit Mix: A diverse mix of credit accounts, such as credit cards, loans, and mortgages, can positively impact your score.

Impact on Creditworthiness

The pivotal role of your FICO score lies in determining your creditworthiness. This numerical evaluation assesses the risk associated with lending to you, with a higher score signifying lower risk. Consequently, qualifying for loans, securing mortgages, and obtaining credit cards with favorable terms, as well as lower interest rates become easier when you boast an elevated rating. Conversely, a lower score may trigger elevated interest rates or potentially the refusal of credit. Thus, the significance of preserving an exemplary FICO score cannot be overstated. It is essential not only for seizing financial opportunities but also for guaranteeing favorable borrowing terms. This highlights its criticality in our economic landscape.

Your FICO score extends its influence beyond lending decisions to other aspects of your financial life. When landlords screen potential tenants, they often inspect their credit scores. Higher scores reflect increased reliability in rent payments. Moreover, insurance companies might consider the individual's credit score as a risk assessment for providing auto or homeowner's coverage. This could consequently impact policy premiums. Actively managing and improving your FICO score over time underscores the importance of understanding its broader implications.

- Interest Rates: Higher FICO scores typically result in lower interest rates on loans and credit cards.

- Employment Opportunities: Some employers may review credit reports as part of the hiring process, particularly for positions involving financial responsibilities.

Maintaining Financial Health

Your financial habits and responsibilities are reflected in a FICO score. Understanding the calculation process and the significance of this score equips individuals to proactively maintain or enhance their financial health. They should strive for timely payments and keep credit card balances low. Avoiding unnecessary credit inquiries is also crucial. Regular monitoring of credit reports to identify inaccuracies or fraudulent activities completes an essential routine at this level of management. Individuals can safeguard their creditworthiness and achieve their long-term financial goals by prioritizing financial responsibility.

Besides implementing these proactive measures, one must crucially acknowledge potential pitfalls that can impact their FICO score negatively. For example, the closure of old credit accounts may abbreviate your credit history and subsequently reduce your score. Likewise, requesting multiple credit accounts within a brief period could indicate financial distress to lenders; this may result in a temporary decline in your score. Manage your finances with mindfulness of these factors. This approach will bolster not only your FICO score but also enhance your overall financial well-being.

- Credit Inquiries: Limiting the number of credit inquiries can help maintain a stable FICO score.

- Authorized Users: Becoming an authorized user on someone else's credit card can impact your FICO score, depending on their payment history and credit utilization.

Monitoring and Improving Your Score

It is imperative to regularly monitor your FICO score for informed credit standing. Free access to FICO scores forms part of the services many credit card issuers and financial institutions offer. Furthermore, several online platforms extend their service offerings with credit monitoring services that enable individuals to track changes in their scores over time. Several strategies exist for improving a lower-than-desired FICO score including timely bill payment, reduction of credit card balance, avoidance of unnecessary account openings, and disputing any errors found on your credit report.

Focusing on the improvement of your FICO score necessitates an understanding of the timeframe required to observe substantial changes. Timely payments and responsible credit utilization, as examples of positive financial habits, can progressively elevate your rating over a period. Nonetheless, it is crucial to exercise patience since overnight improvements may not transpire immediately. Prioritizing actions with a significant impact on your score such as addressing delinquent accounts or high credit card balances is essential. By remaining committed to these strategies and monitoring progress rigorously, you can steadily elevate your FICO score and fortify your financial foundation.

- Credit Age: Closing old credit accounts can shorten your credit history, potentially lowering your FICO score.

- Credit Limits: Increasing credit limits on existing accounts can lower your credit utilization ratio, positively impacting your FICO score.

Conclusion

To conclude, lenders employ a FICO score as an essential tool for evaluating an individual's creditworthiness. It is crucial to comprehend the elements that formulate this score and their influence on financial health. Such understanding informs decisions about credit, enabling effective management of personal finances. Through consistent monitoring and active efforts towards the enhancement of their FICO scores, individuals can bolster their standing in terms of credit while paving the way for superior future financial opportunities.

-

Investment Mar 14, 2024

Investment Mar 14, 2024MyWallSt Review 2024: How Does This Stock Picking Service Compare?

Discover if MyWallSt is worth your investment. This review compares its stock picking service, features, and more

-

Taxes Mar 22, 2024

Taxes Mar 22, 2024A Comprehensive Guide to Income Tax Deductions

Uncover essential income tax deductions for 2024. Maximize savings with expert insights on eligible deductions and strategies.

-

Taxes Jan 04, 2024

Taxes Jan 04, 2024Will There Be an Impact on Tax Refunds Due to the Shutdown?

Between December 22, 2018, and January 25, 2019, the federal government in the United States was closed. This closure, which lasted for 35 days, was the longest in the history of the United States. As a result, the services of several government agencies, including the National Park Service, were severely interrupted. Despite this, the Internal Revenue Service did not completely halt operations, as it never does, even when the government is shut down. Many of its workers were furloughed (temporarily laid off), and while some of the company's services were disrupted or delayed, others were not affected. What does this entail for the refund of your taxes?

-

Investment Mar 15, 2024

Investment Mar 15, 2024A Guide to Inverse ETFs: Protecting Your Investments in a Falling Market

Discover how inverse ETFs help investors profit in falling markets.